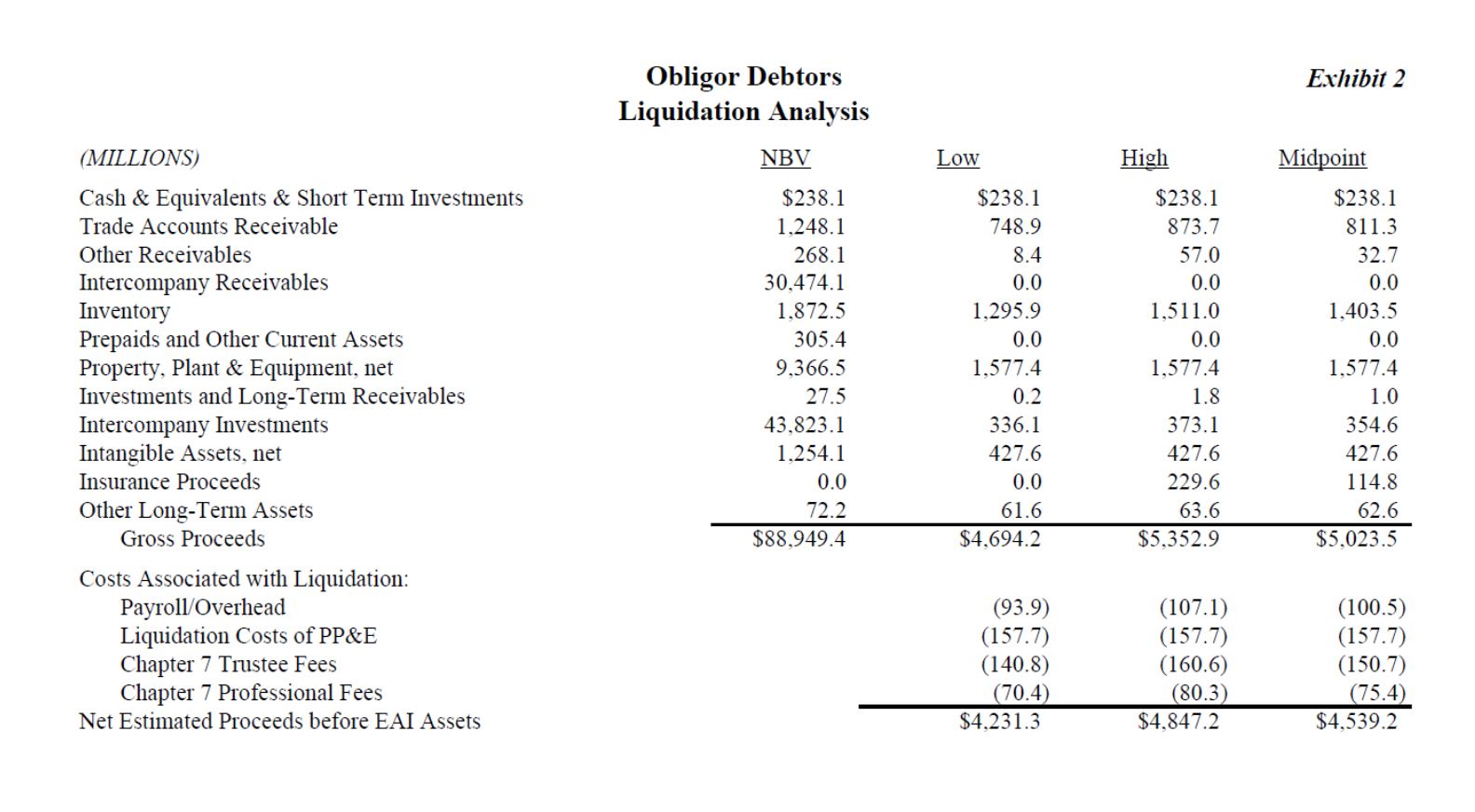

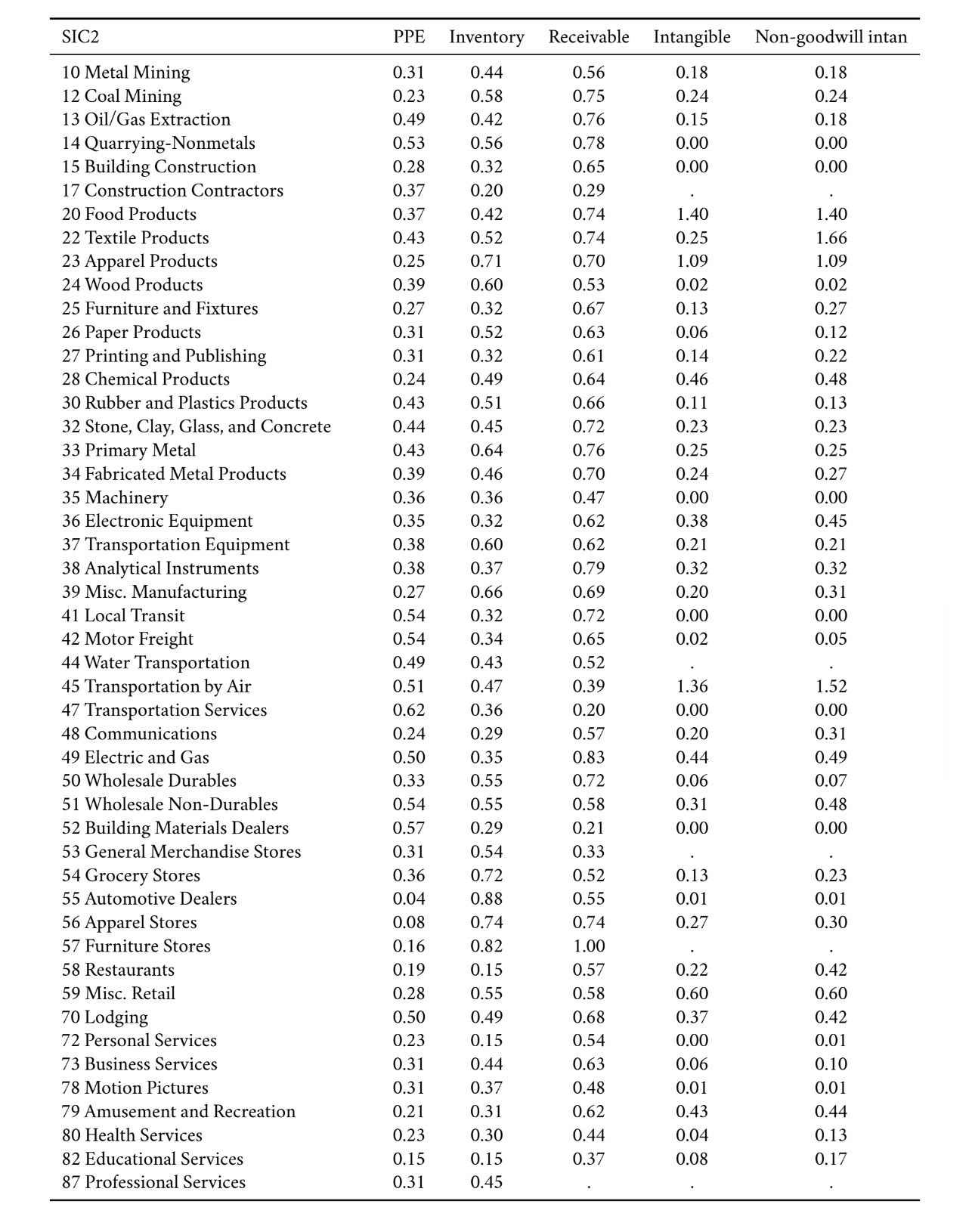

3. Using the industry-level liquidation recovery rate, we can calculate the estimated firm-level liquidation value for firms in Compustat:

where Liq i,t is the total liquidation value of firm i at time t , j denotes the asset type (e.g., PPE, inventory), λ i,j is the industry-average liquidation recovery rate for this type of asset (based on the firm’s industry), and K i,j,t is the book value of asset j for firm i at time t .

where Liq i,t is the total liquidation value of firm i at time t , j denotes the asset type (e.g., PPE, inventory), λ i,j is the industry-average liquidation recovery rate for this type of asset (based on the firm’s industry), and K i,j,t is the book value of asset j for firm i at time t .

where Liq i,t is the total liquidation value of firm i at time t , j denotes the asset type (e.g., PPE, inventory), λ i,j is the industry-average liquidation recovery rate for this type of asset (based on the firm’s industry), and K i,j,t is the book value of asset j for firm i at time t .